Welcome to the Road Ahead for Automotive Retail Report

2025

In last year’s inaugural event and Report, we looked in depth at the major CASEDD (Connectivity, Autonomy, Subscriptions, Electrification, Digitalisation, Distribution) related themes and forces of change which are posing the biggest and most imminent disruption for retailers.

In this second edition, and over the course of several weeks, we’ll be revisiting some of those themes in detail, evaluating how they’ve evolved over the last 12 months, and identifying which require your attention in 2025. Using an in-depth study of over 80 retailer groups conducted exclusively for Auto Trader by the US’ leading independent automotive researcher, Glenn Mercer, we’ll be exploring what this market wide disruption means for your business, and how you could adapt accordingly.

We’ll also reveal the findings of our own in-depth analysis of over a million different data points from thousands of international retailers investigating how businesses can more effectively measure profitability, and how they can unlock more from their teams.

In this first chapter, you’ll find an executive summary of the findings and the insights shared at this year’s event, attended by over 200 leading franchise retailers, followed by bi-weekly instalments diving into the results in detail. In each, we’ll be revealing why returning to operational basics and concentrating on the factors you can control within your business will be essential in today’s retail environment, and how measuring your performance effectively may be the key to unlocking more profitability.

Of the six CASEDD themes explored last year, there are three immediate trends that are set to have the biggest impact on retailers in 2025, particularly franchise businesses which will be the first to feel their impact: electrification, distribution and digitalisation. Whilst all of these themes present their share of challenges, as Ian Plummer, Auto Trader’s Commercial Director highlighted during the event, they also represent unique opportunities.

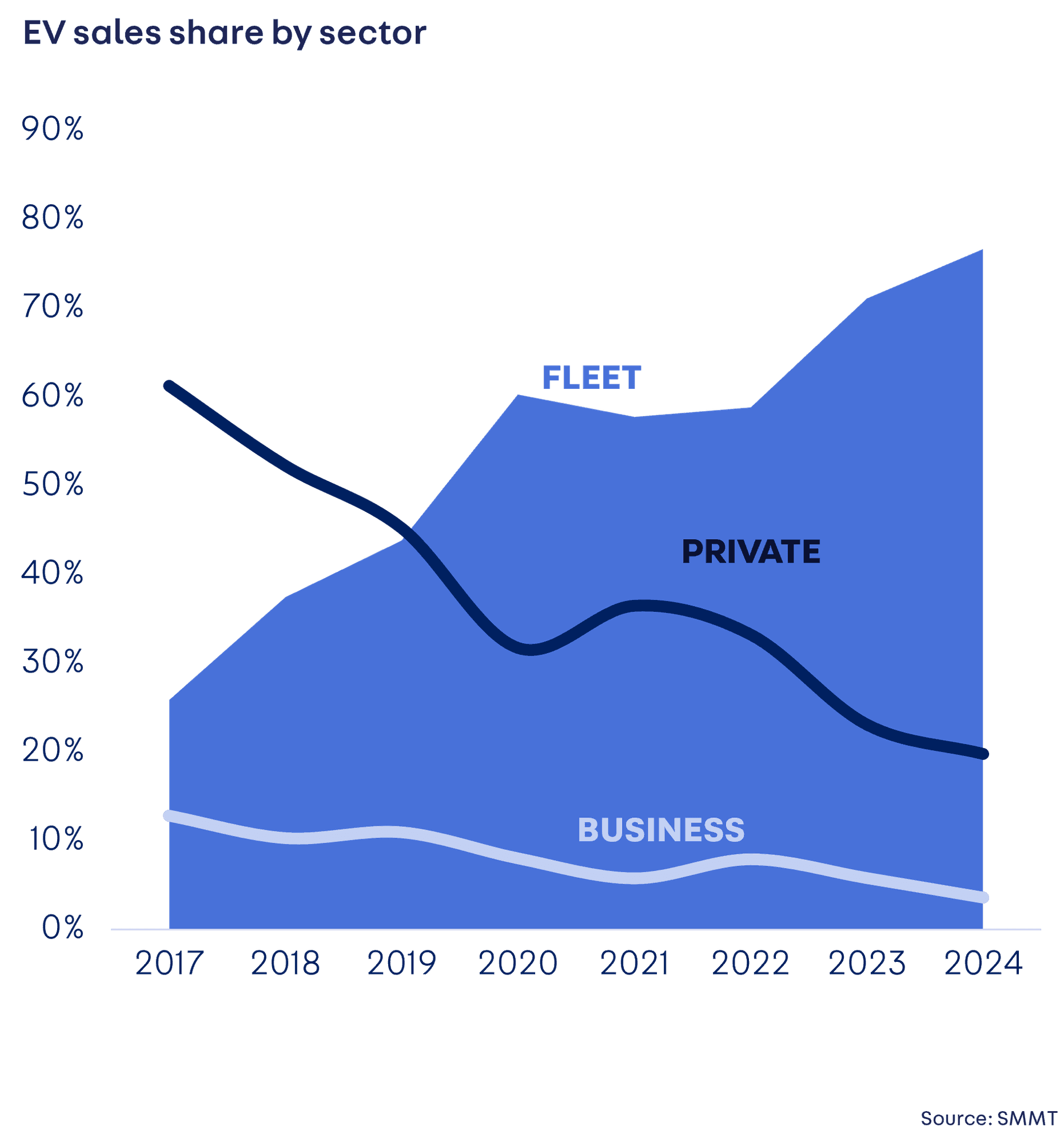

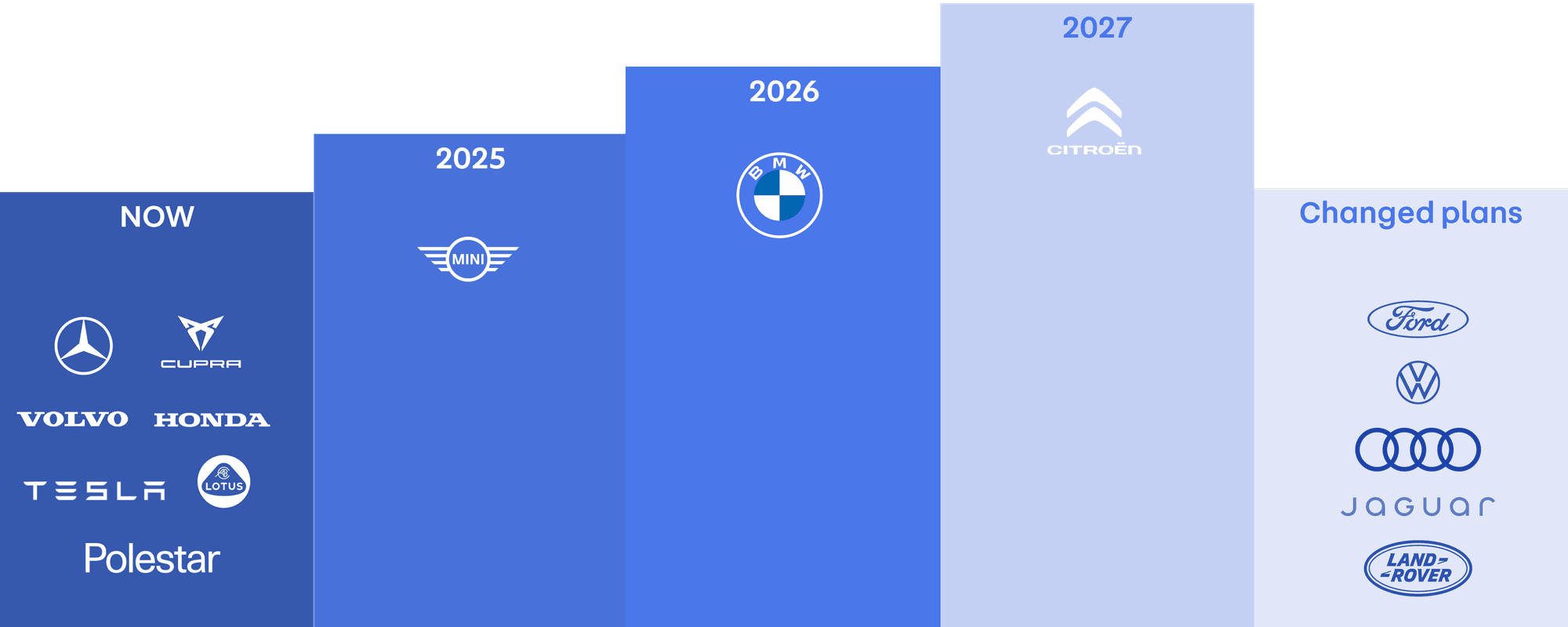

2024 was the year of ‘peak petrol’ – from now on the volume of petrol cars on the UK’s roads will fall – and a record year for electric. Electric share of new car registrations hit 19.6% with the volume approaching 400,000. However, progress came at a cost in the shape of heavy discounting (estimated at £4.5bn) whilst Fleet sector dominance (3 in 4 EVs registered) will present challenges. The shift to electric is also fuelling an erosion in brand loyalty (EV buyers are half as likely to buy from the same brands as ICE buyers) at a time of increased competition, with over 70 brands expected to be in the UK market by the end of the year (up from 47 in 2020). Despite these hurdles, there are significant opportunities for retailers. The shift in loyalty offers a chance to capture new customers, and by identifying which brands are best positioned to grow market share, retailers can attract new buyers and boost renewals, enhancing their market presence.

While some brands have reconsidered their plans in light of market conditions, the agency model is far from abandoned. Some have adapted their original ambitions from ‘full agency’ to a ‘Franchise +’ approach; a hybrid partnership between manufacturer, retailer, and marketplace, which allows the retailer to benefit from the agency model while maintaining market share.

Of all the three themes, digitalisation perhaps represents the biggest opportunity for retailers, in terms of both driving efficiencies, and enhancing the consumer experience. On this point, Ian highlighted that as choices have become more complex, the demand for an omni-channel journey that blends digital convenience and transparency with the in-person experience that only a retailer can offer, is accelerating.

This 'digital first' mindset (evidenced by nearly a billion visits to Auto Trader last year) and the right online presence is also influencing footfall - although some consumers contact a retailer before visiting, the majority still just walk in, looking to speak to someone before finalising their purchase. Three quarters of walk-ins don’t feel the need to make contact first having already researched the car and retailer – online for consideration, showroom for validation.

An OC&C study showed that 60% of sales team tasks could be made more efficient or even be replaced by technology. It highlights the huge operational efficiency opportunities that advancements in digital technology represents.

In the next chapter of this report, we’ll be exploring these CASEDD related themes in detail, revealing how instead of being just challenged by them, they can be used to reshape your business to become more successful.

Clearly the market is moving quickly. And it’s not just CASEDD forces of change which retailers are having to navigate. Retailers are also facing the challenge of shifting market dynamics and consumer behaviours, as well as an underperforming new car market, and, despite very strong levels of demand, a used car market stifled by a shortfall of stock.

To understand how retailers can still drive profitability and sell cars within this landscape, Auto Trader worked with renowned US automotive researcher, Glenn Mercer, who conducted an in-depth study of more than 80 UK franchised retailers. At this year’s event, Glenn revealed his findings (which we’ll be sharing in-depth in a future instalment) and asserted that retailers on both sides of the Atlantic need to adopt a ‘back to basics’ approach; to focus on the factors they can control ‘within their walls’.

His research highlighted a conservative outlook among UK retailers, with profitability expected to remain largely flat (1.5-2%) across all key operational departments: Aftersales, Finance & Insurance, New Car, and Used Car. There were bright spots in his findings, however, particularly in the used car department, which was recognised as offering the biggest opportunity to recover profits lost in the new car department.

Glenn Mercer presenting at The Road Ahead for Automotive Retail event 2025

Traditional solutions to improving profitability (aggressive pricing, competitive part-exchanges etc.) are no longer possible: margins and market dynamics are tough, car buyers are highly informed, competition is more intense than ever, and market volumes are unlikely to increase significantly, which limits the opportunity to increase profit by selling more.

Mercer explained that the path to better profits, therefore, lies in operational excellence - to ‘out-retail’ your competition, rather than trying to ‘out-deal’ them.

He identified broad tactical and strategic themes that time and personnel constrained retailers are prioritising to improve profitability, including retention, cost reduction, and achieving scale.

The biggest lever to profitability however, was (finally) unlocking ‘the promise of IT’ – however, before investing in the cost of new technology, reviewing processes and people, and how technology will make them more efficient is essential.

The ability to ‘out retail’ relies on how effectively retailers can measure performance and their subsequent profitability. Having the right Key Performance Indicators (KPIs) in place are crucial, but Mercer questioned whether you can have a key performance indicator if you have dozens of them. He identified a list of 30-40 KPIs UK retailers are using across operational departments, suggesting a lack of clarity on what should be measured.

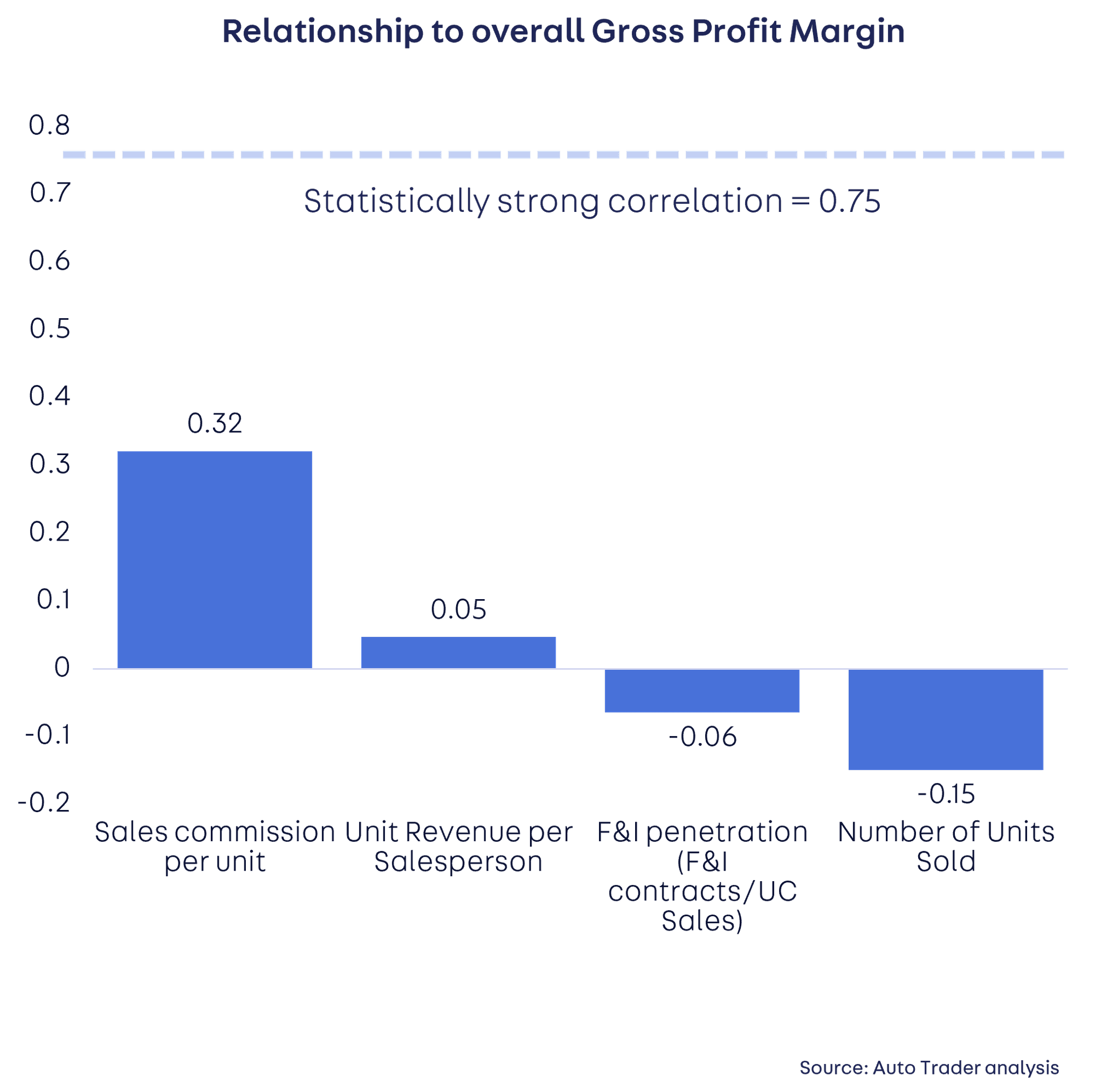

So, what KPIs should retailers be measuring? Is there a simple metric that determines profitability? According to Marc Palmer, Auto Trader’s Head of Strategy & Insights, who revealed the findings of an Auto Trader analysis of more than a million data points from over 2,500 international retailers, the answer is no. Surprisingly, most KPIs have no relationship to Gross Profit Margin, and in isolation common metrics have little impact. The analysis did reveal however, many inter-relationships between the different metrics; combinations which provide a better guide to departmental profitability, and an opportunity to balance volume and profit, rather than focusing on volume alone.

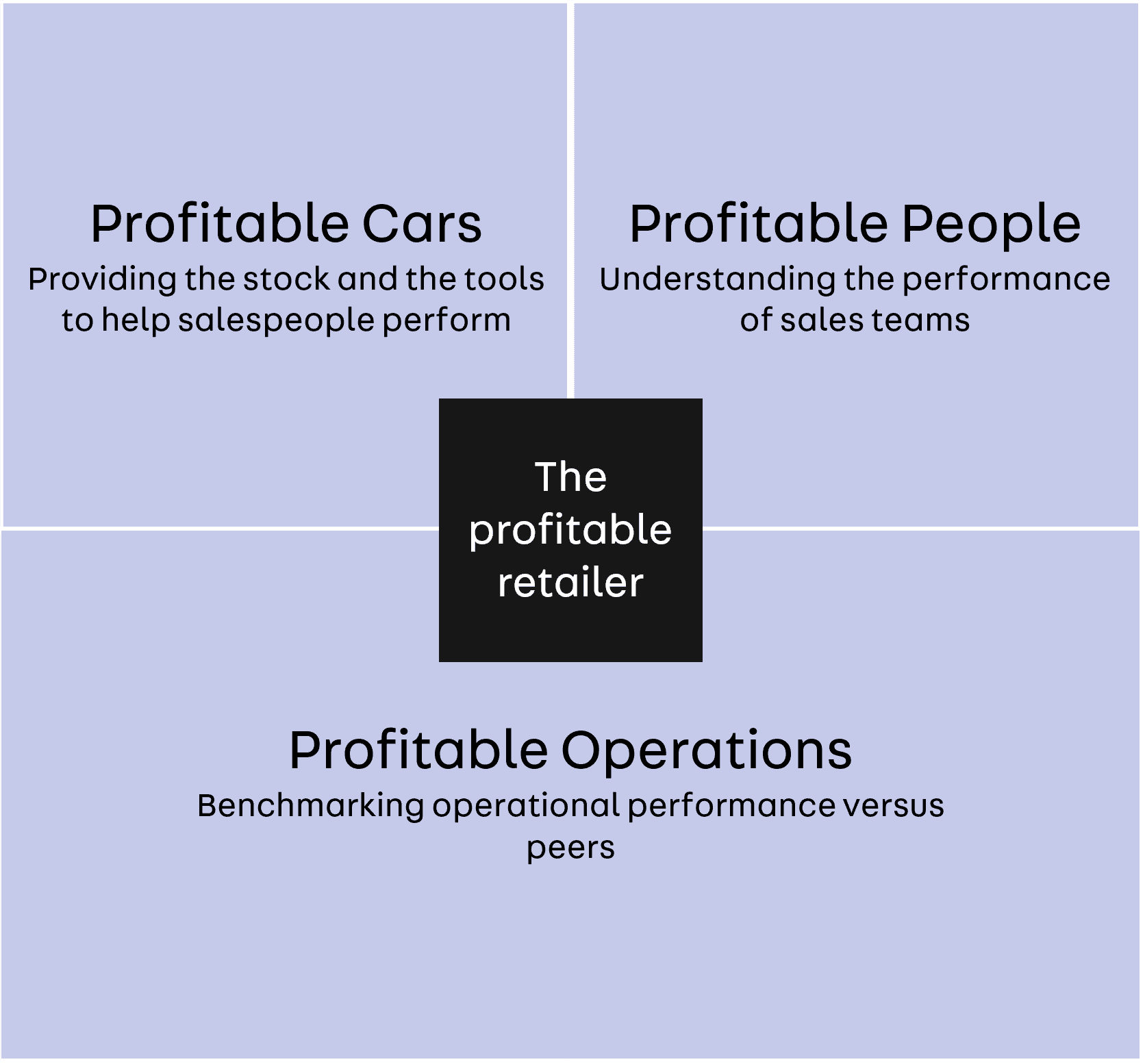

To illustrate how understanding these relationships may offer the key to driving growth, Auto Trader focused on measuring profitability in the used car department, which Mercer’s research highlighted as the best opportunity to recover lost new car profits. The analysis looked at the metrics of three key components of what makes a profitable used car retailer: profitable people, profitable cars, and profitable operations.

We examine each in detail in the fourth chapter of this report, but during the event we focused first on profitable people – the impact of people on profit. The findings of the analysis revealed an important relationship between volumes, people (sales and non-sales) and revenue in determining profit per salesperson per unit, a far stronger guide to overall gross profit margin than any other metric, including sales per salesperson.

We also heard how to ensure retailers that retailers have profitable cars on their forecourt. Research shows that there is more profit to be gained from the metal and how a combination of the right metrics and tools hold the key to ensuring that pricing levers don't need to be pulled to drive sales.

Finally, we unveil an all new project to help retailers determine how profitable their operations really are with an all new set of KPIs.

What does all of this mean for the future of automotive retailing? Last year Auto Trader explored the big forces of change that would shape the market for years to come – electric, agency models, and the fact omni-channel killed online - and concluded that within the midst of all this change, the role of the retailer was more important than ever because they’re the closest contact point with the consumer.

What’s going to shape 2025 and beyond for retailers? Market forces haven’t changed significantly: electric remains the future, but it’s about how quick we can embrace the opportunities that come from that transition. It’s also about data AND insights: but how do you distinguish between a key performance indicator, and simply a performance indicator, how do you benchmark? That’s about bringing the best of human intelligence, with the best of data and AI and technology. And rather than omni-channel killed online, we’re now in a world where omni-channel isn’t optional. It’s the consumer journey that all retailers are experiencing to one degree or another, and it’s the industry’s job to support consumers though the retailing journey the best way they possibly can.

In her concluding comments, Auto Trader’s Chief Operating Officer, Catherine Faiers, agreed that to drive profitability businesses must ‘reset the basics’, and drive the metrics that can be controlled – retention, cost reduction, and leveraging the promise of tech. It’s those retailing capabilities that will differentiate in the future:

“It’s not about being the best possible version of a dealer you can be anymore, it’s about evolving from dealing to retailing, and it's retailing excellence that will differentiate how businesses perform in the coming years. There’s no silver bullet or metric, but understanding what you think those measures of success are for your business and measuring them will be key.

“The Road Ahead for Automotive Retail will look different, but with it will come opportunities to redefine and reshape the role of the retailer, to move on from dealing excellence to a world shaped by retailing excellence. So, as well as a decade for change, and evolution it’s also a chance to build businesses we want for the next decade, which will require planning, action, and insights, and we’re here to help you at every step of the journey.”