The case for CASEDD

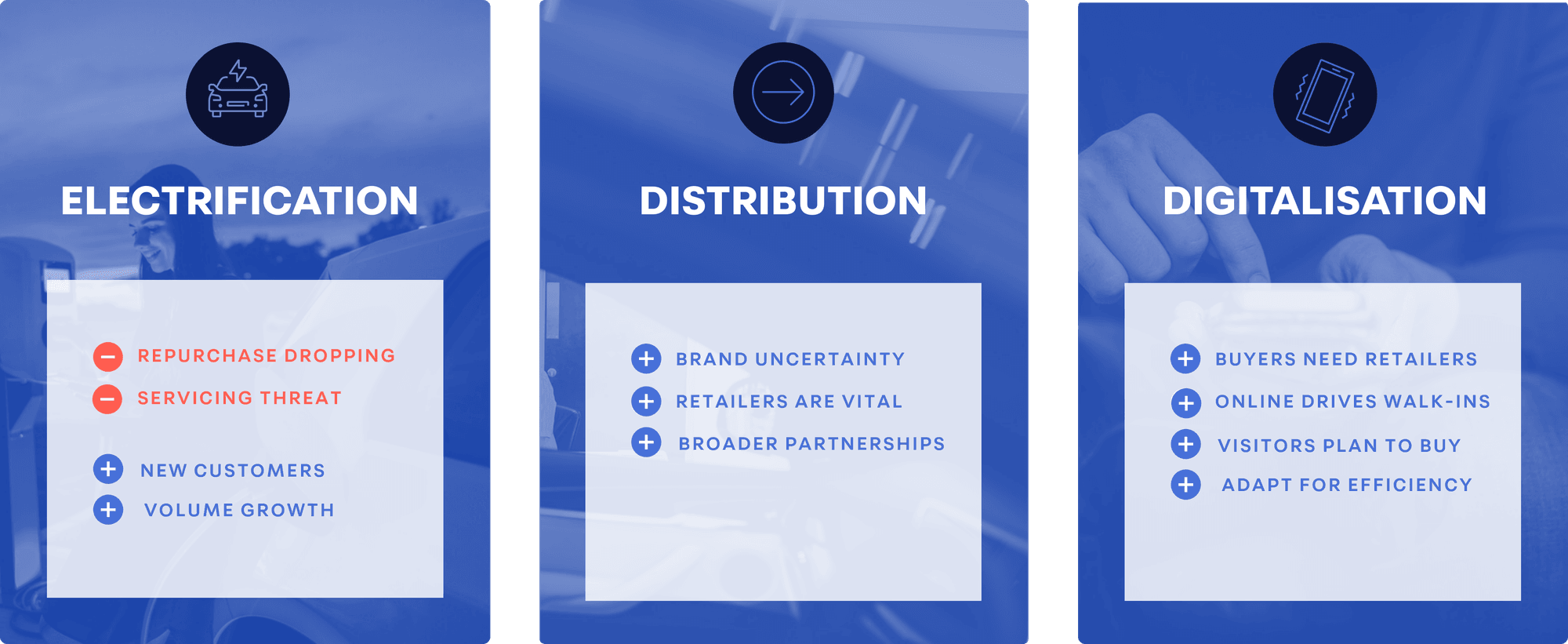

Of the six CASEDD themes, there are three immediate trends that are set to have the biggest impact on franchised retailers this year: electrification, distribution and digitalisation. Each of these trends will have a varying degree of impact on retail in the near term.

Progress, but at a cost

2024 was the year of ‘peak petrol’ and a record year for electric. Electric share of new car registrations hit 19.6% with volume approaching 400,000, driven by heavy manufacturer discounting - estimated to have cost £4.5bn - and the Fleet sector, which accounted for 3 in 4 new electric cars. From now on the volume of petrol cars on the UK’s roads will fall

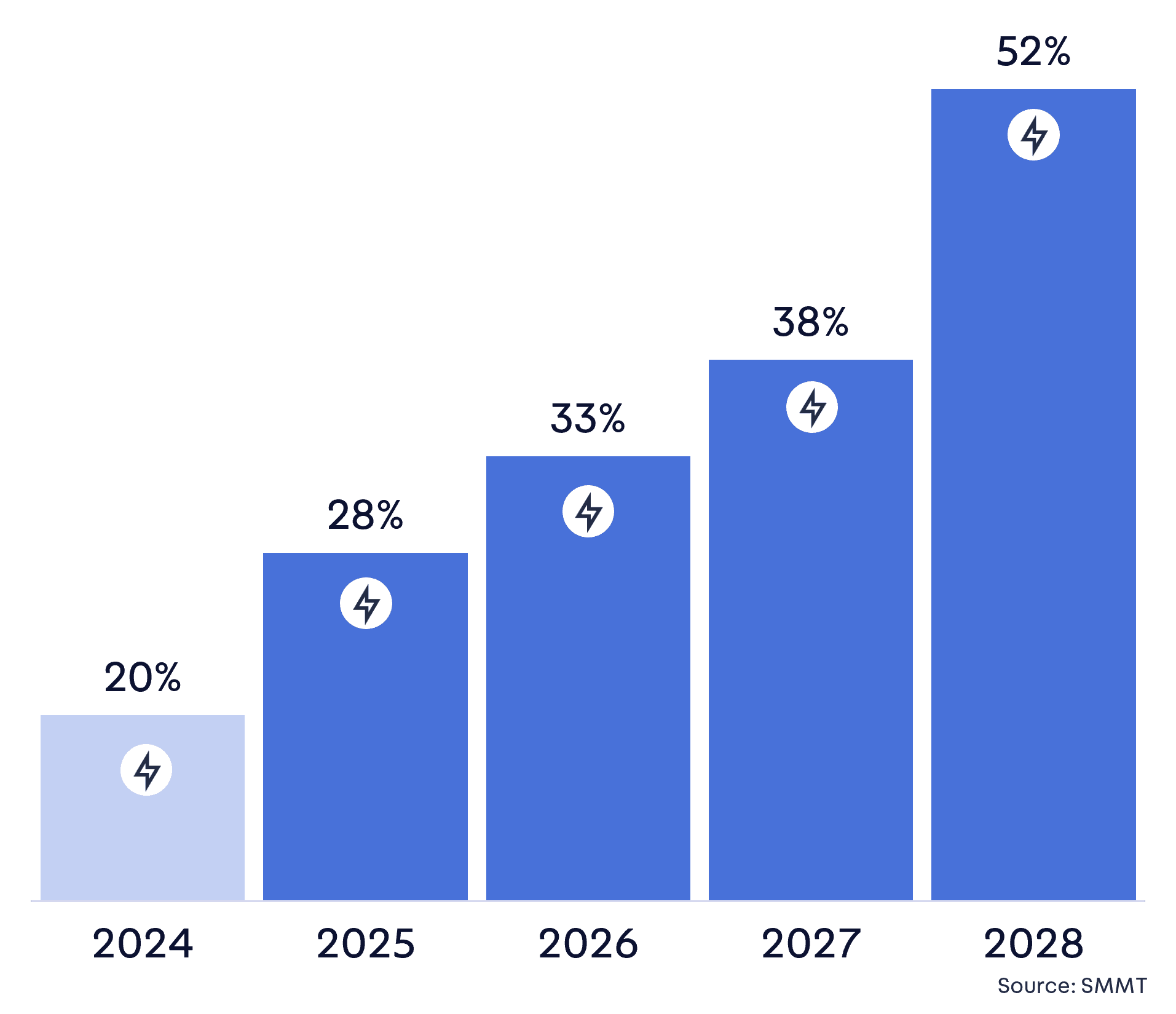

The ZEV Mandate’s path to 2028 is steep

Switch into other channels

3 in 4 new EVs are registered via the Fleet sector – only 1 in 10 Private sales is electric. Nearly half of all EV registrations were via the Contract Hire / Leasing channel, in 2024 driven by BIK savings and salary sacrifice schemes - a further 15% were to Motability drivers.

These drivers are often unknown to the brand and retailer – the PCP renewal cohort is reducing.

Repurchase rates, service revenues and part exchange volumes are uncertain.

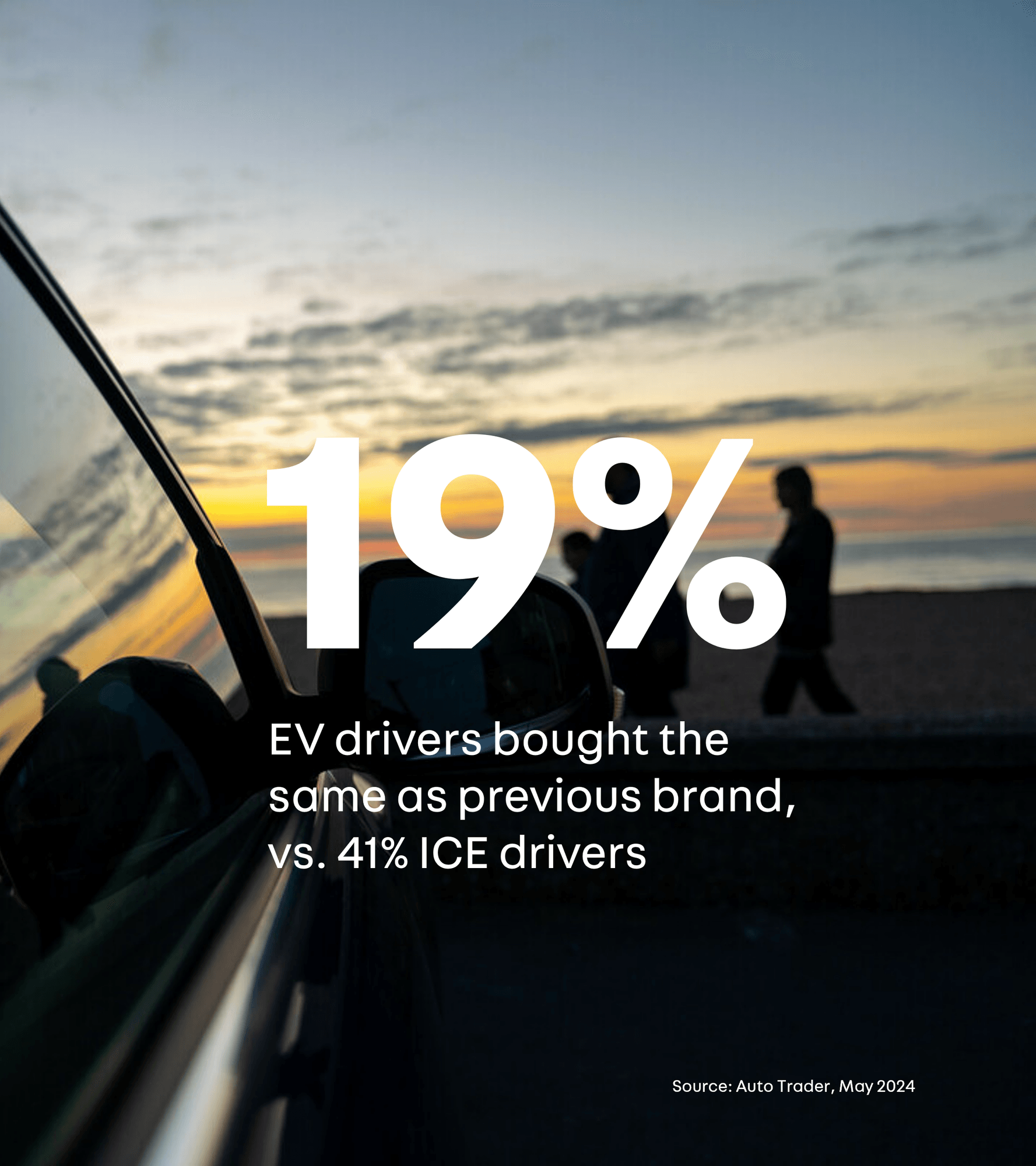

Electric’s erosion of loyalty

New EV buyers are only half as likely to buy from the same brand.

Historically, brands, retailers and captives have been able to rely upon loyalty rates of 40% or more.

But electric is different. Buyers are more open to different brands, supply forced some to look elsewhere, and salary sacrifice schemes widened choice and shortlists.

The opportunity to attract and acquire new buyers has opened.

Choices from China

By the end of the year there will be 65 brands selling cars in the UK, up from 47 just 5 years ago. New entrants from China will add greater competition, but not incremental market volume – incumbent brands will lose share. But the opportunity in multi-franchising is the greatest it has ever been, bringing new products, buyers – and volume.

These developments will present some challenges for retailers, but critically they also present some huge opportunities too, to pivot from loss to gain. Waning brand loyalty may mean a reduction in repurchases for example, but it also represents a unique chance to capture new customers from competitors. By identifying which brands are best positioned to grow their market share and leveraging this knowledge, retailers can successfully attract new buyers and increase renewals, ultimately boosting their market presence.

Last year, we highlighted the relatively limited success of the agency model, with many manufacturers scaling back their original plans. But whilst some agency moves have slowed, it would be a mistake to think the model has been abandoned altogether. The significant pressures that galvanised OEMs to evolve their distribution channels remain ever-present, and a number of brands have found ways to make it work. However, the huge value of the retailer remains unchallenged.

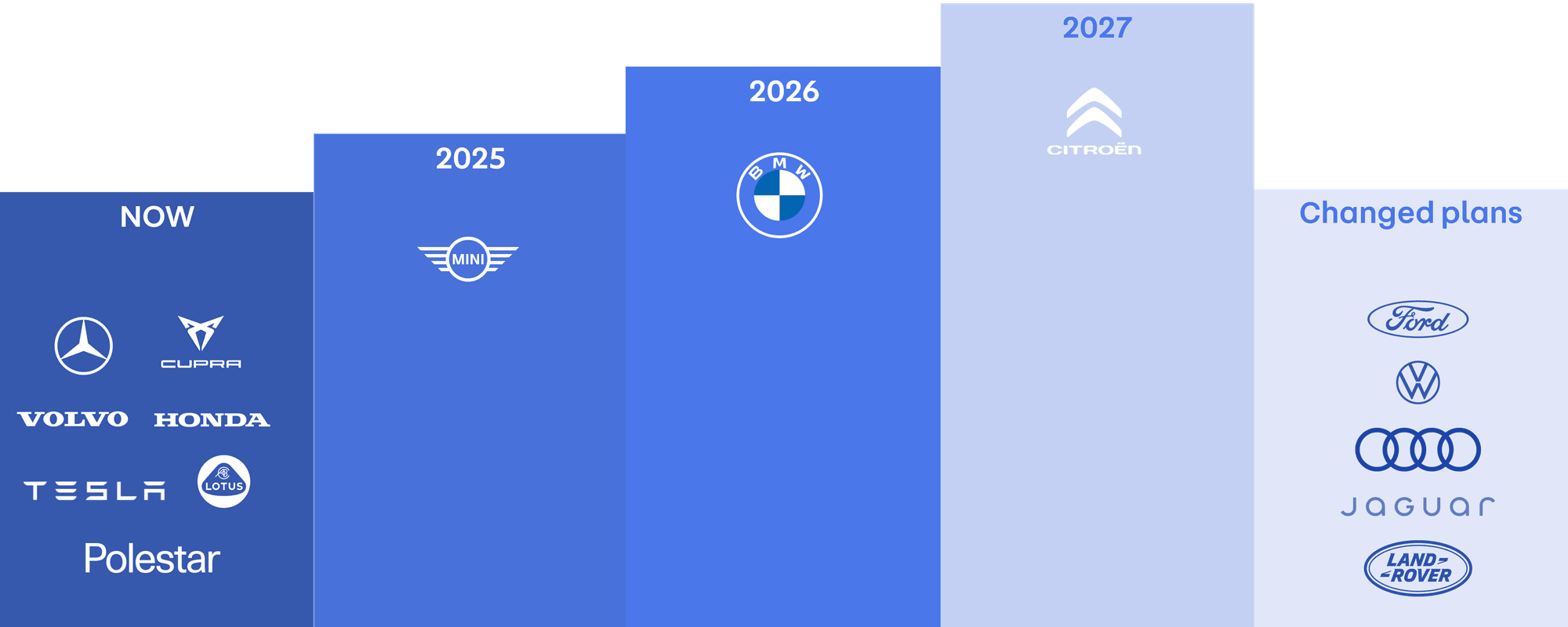

Some big brands have changed plans: Some persevering, some postponing, …it’s not clear what’s going to happen.

Competition is intensifying: More than 70 brands are now in the UK, creating a challenging landscape.

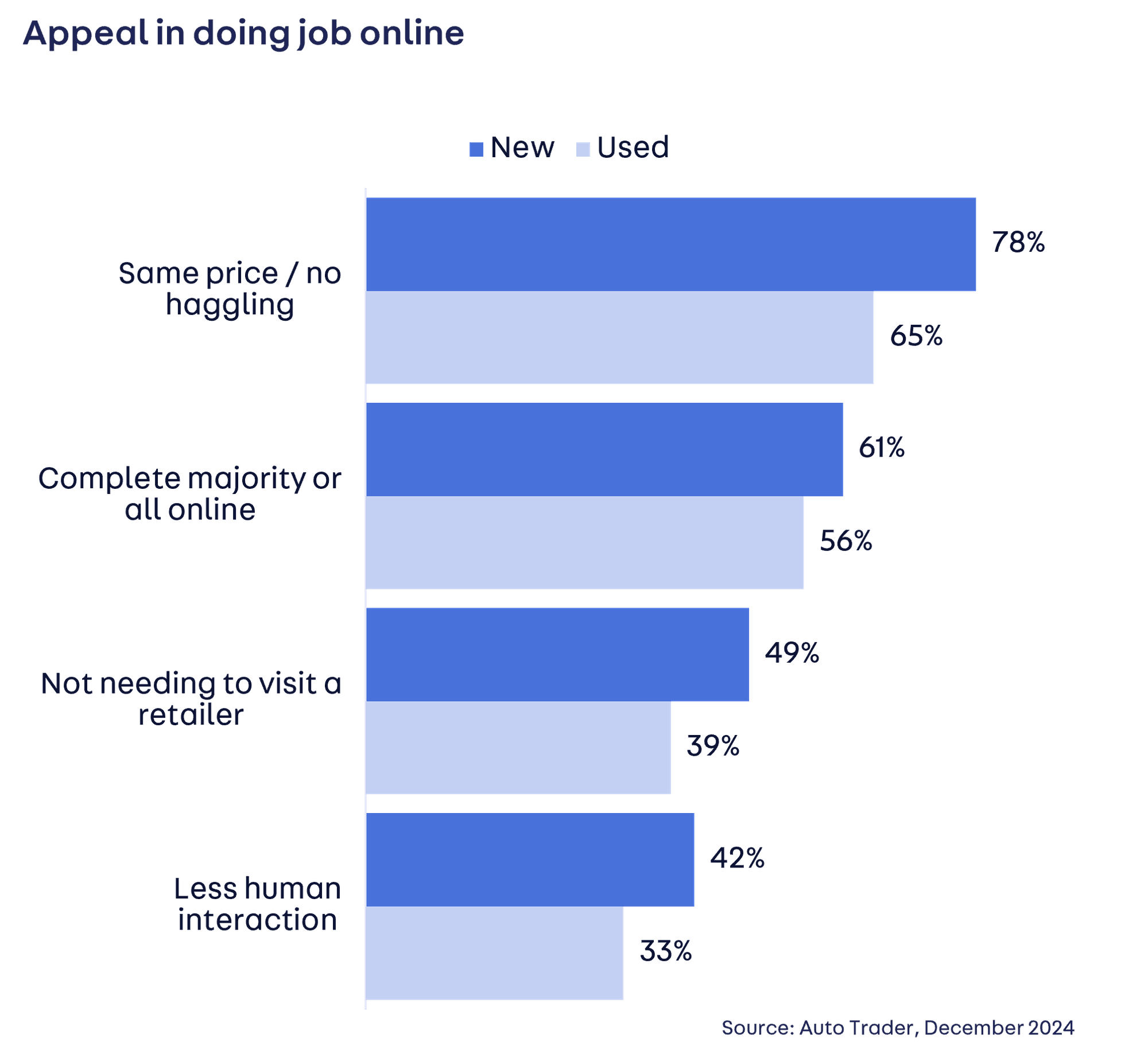

Pure online still lacks high appeal: Consumers still have significant doubts about buying a car fully online. Consideration is higher for new car buyers, with 52% willing to consider buying a car online vs just 38% of used car buyers, but at just over half of the private market the opportunity is limiting. Manufacturer plans have had to evolve, balancing sales volume targets with a weaker market and slower consumer acceptance. For manufacturers, the retailer remains important. Success in Franchise +: Having changed approach, some brands have taken a different partnership route in a middle ground. Distribution costs are reduced, consumer transparency is increased, and brands and retailers are rewarded through broader partnerships.

Brands are changing their plans, but the agency model takes time and preparation, and it seems the market conditions need to be right for it to work. Crucially, car buyers still want to buy from people, as pure online retailing has yet to gain mass appeal (although new car buyers are more interested). The partnership between manufacturers, retailers, and marketplaces is working for some big brands, which suggests it’s possible to gain some of the benefits of the agency model and maintain share.

The impact of digital on the consumer experience has been significant, and with nearly a billion visits to Auto Trader in 2024, an additional 180 million in just two years, the ‘digital first’ mindset among car buyers is clear. But while more people are open to buying a car exclusively online, the majority prefer a blended retail journey, combining digital ease and transparency with an in-person experience that only a retailer can offer.

Retailers are unlocking greater reach and efficiencies by embedding digital products and services, but it’s the hybrid process that holds the most potential. This seamless and connected buying experience across channels helps grow their audience, improve customer service, and enhance operational efficiency. Thus, the hybrid approach not only benefits car buyers by catering to their evolving needs but also positions retailers for future success, ensuring they remain vital in the ever-changing market.

Online replaces tasks, not talking

Online should make some jobs easier and transparent as choice becomes more complex. Price consistency across the country and transparency are most appealing, especially on new cars, but online appeal weakens as they get to the more involved jobs. For buyers, the retailer is more important than ever.

Omnichannel isn’t optional

Growth in pre-contact, but the majority still just walk in. Three quarters of walk-ins either didn’t see the need to make contact or found it just as easy to stop by. Most have done their research into the car and the retailer and don’t submit a lead – whether new or used, enquiries remain the minority.

6 in 10 visitors plan to buy

59% of buyers who hadn't submitted a lead say they plan to buy from the retailer, either on the day or later on. Most (69%) said it was the first time they’d visited the retailer, and over half don’t plan to visit anywhere else. The retailer visit is moving ever closer to a single-shot verification of a decision made online. Online is therefore for consideration, with a visit for confirmation.

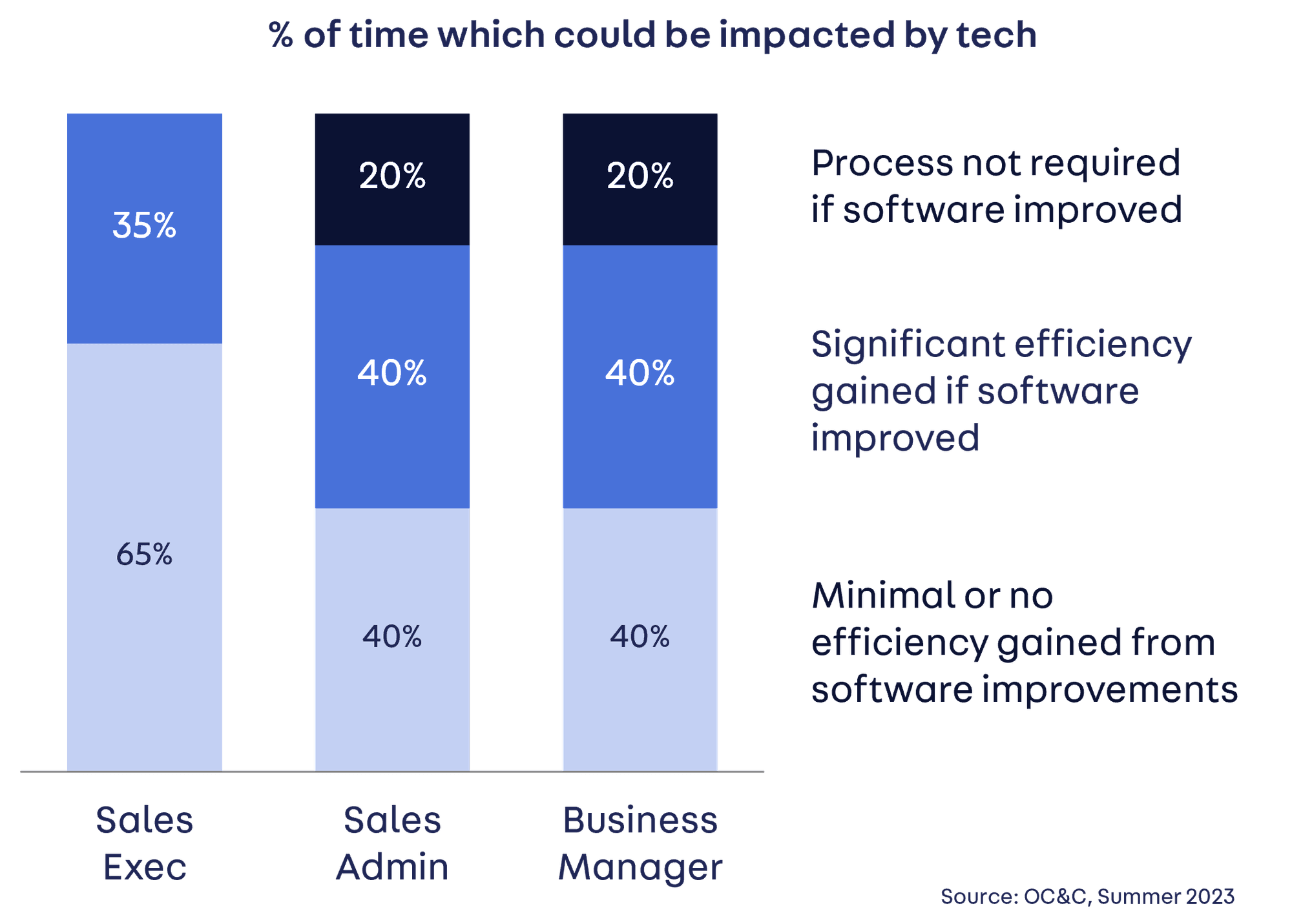

Operational efficiency? Not yet

Up to 60% of sales team time is ineffective. Technology is the key opportunity for realising operational efficiencies. Where to place strategic focus, how to apply technology, how to change people and processes and how to measure impact are yet to be fully understood. Critically, it’s important not to add additional technology costs without first adapting people and processes

To conclude these three themes: in all the research we do, we think each of these three equations throws up challenges, but if you seize the opportunity and fully understand the risks involved, and can mitigate those as well as leverage the opportunity, they create an ability to reshape your businesses and become more successful than in the past, rather than just be challenged by these things coming at you.

Yes, electric vehicles pose a threat in many ways, but they do open the door to new customers and new brand partners. Distribution models have been challenging, and they still are, but they are opening lines and there is an open door between brands and their retail partners, which creates an opportunity to reshape the model to suit both parties. In terms of digitalisation, there are plenty of opportunities to leverage that can reshape businesses, partly to improve efficiency. But arguably more important is the need to focus on the value add we’re providing consumers who seek out a hybrid journey.